Not all residential rental property interest is deductible (sponsored content)

Nigel Smellie - Financial Contributor

21 August 2022, 4:15 PM

Last month we explored the impact of changes to the Bright-line rules Accounting: Are you confused by the Bright-line Test? which were one part of recent government property tax changes.

This month, we explore the second part which relates to the changes of interest deductible on residential rental properties.

The purpose of these changes by the government were largely to close a “loophole” in the tax rules, help cool the housing market, and push property investors towards (exempt) new builds to free up existing housing stock for first home buyers.

In practice, owners of affected residential properties won’t be able to claim an interest deduction from 1 October 2021, unless otherwise exempted.

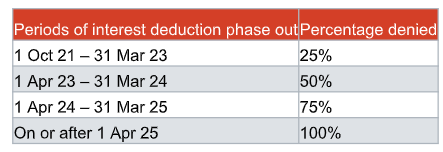

This limitation will either be a fully interest denial, if the property is acquired on or after 27 March 2021 (unless exempted), from 1 October 2021.

Whereas for properties acquired before this date, interest can still be claimed for a few more years, however, there will be a reduction in how much can be claimed as outlined in the below table:

Exemptions

The main exemption is when the property is considered a “new build”.

A “new build” is when a place is added to the land which is configured as a self-contained residence or abode. Evidence of this construction via a code of compliance certificate (CCC) issued on or after 27 March 2020 is generally required.

For these properties,100% of the interest cost on loans relating to the property remain deductible for a period of 20 years from the date the CCC is issued, to the extent that the loan relates to a new build. This applies no matter who owns the property. An apportionment might be required is the “new build” is being added to land that already contains a residence.

Therefore, if you are looking to purchase a residential rental property via a loan, we’d suggest undertaking some due diligence to determine if the property meets the “new build” criteria and from when.

Although the tax impact should not be the only consideration when comparing new and established builds, you need to do your research around the impact of loan terms, interest rates, and marginal tax rates.

As with the Bright-line test, these rules are unfortunately complex. Receive the right advice regarding the potential interest deductibility impact for your circumstances by contacting [email protected]

Findex NZ Limited trading as Findex.

The views and opinions expressed in this article are those of the author/s and do not necessarily reflect the thought or position of Findex NZ Limited.

See our disclosure information on our website https://www.findex.co.nz/disclaimers/disclaimer-and-disclosure

NEWS

FREE ADVICE

ROADS